For a moment, consider our customers to be the “architects of their dreams”. And then think how we could be a partner in their efforts to realize their goals and passions?

It’s actually a question of survival that doesn’t leave much choice. Banks must morph from being a facilitator of financial transactions to being a partner that helps customers achieve our dreams. We are at an inflection point. As consumer interactions and behavior become more connected across industries, and across channels, it is extremely important for banks to continue evolving their view of the consumers and embed themselves deeper into the entire experience cycle.

One of the primary ways to achieve this is through creating a contextual and personalized ecosystem. This statement implies that we understand and act upon customer and partner perspectives throughout their experience lifecycle and life-stages, taking into consideration both direct and indirect customers. In essence, we must build a community. Effective community development can directly drive key parameters such as acquisitions, account growth, cross sell and retention.

One of the primary ways to achieve this is through creating a contextual and personalized ecosystem. This statement implies that we understand and act upon customer and partner perspectives throughout their experience lifecycle and life-stages, taking into consideration both direct and indirect customers. In essence, we must build a community. Effective community development can directly drive key parameters such as acquisitions, account growth, cross sell and retention.

How could we define an ecosystem that will expand the boundaries of relationship management and customer engagement? Can we create a community of “customers” – retail banking customers, merchant customers, partners, and indeed the much wider marketplace of providers and consumers?

Defining the “Community”

In this context, a community is a coming together of consumers and service providers to satisfy mutual needs. For our purposes, a community is not defined as a group characterized by sharing of common values or even collaborating with or helping each other. To do that would be to limit it to a partial dimension. Instead, a community is a coming together of people with different motivations. The structure of what we do with the community defines the context of what it is.

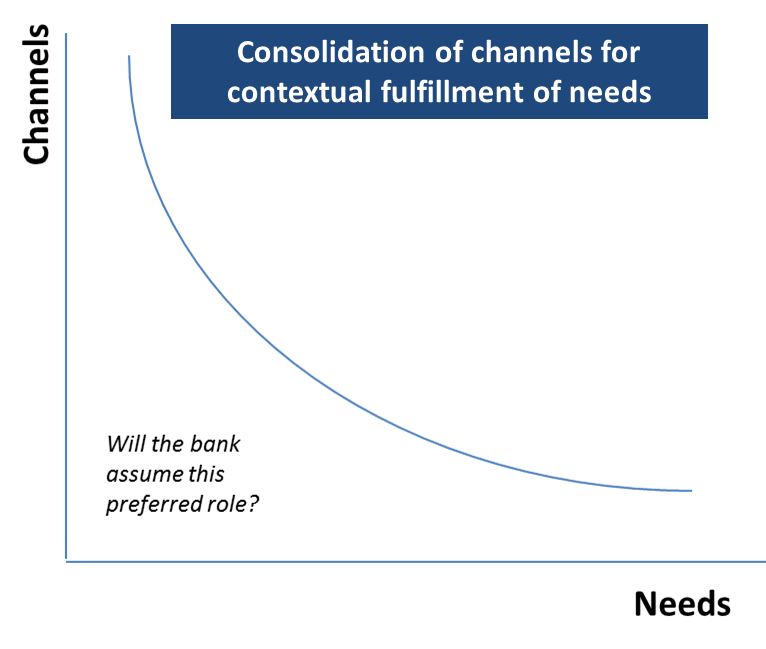

It is important to note that an organization as diverse as a financial services organization has not one target segment but many. Indeed, the product, marketing and service models are numerous as required to serve and satisfy these segments. Further, banking being an integral part of society, and an area that is being addressed by several non-traditional players, must develop a product and services partner ecosystem. Only such as ecosystem will allow customers to truly interact and engage across their needs spectrum while minimizing the mediums over which they interact.

The key question for the emerging marketplace is: Which banks will retain their traditional customer facing dominance and who will be relegated to being back end “essential” service providers?

The social face of the bank

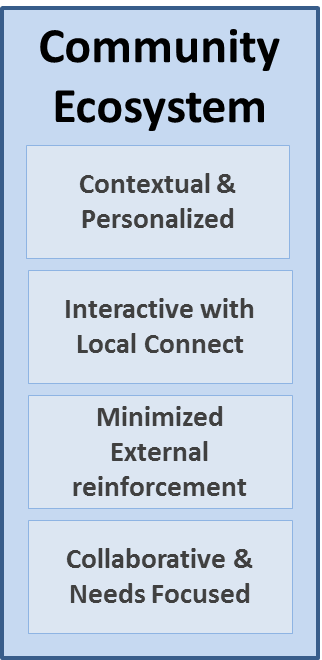

The social face of the bank can be viewed as a set of core capabilities focused on creating an ecosystem of customers and partners and enabled through a set of supported capabilities. The ecosystem will be characterized by:

- Minimizing external reinforcement which implies

- Encouraging the users (consumers, customers and partners / merchants) to promote the community as a destination for needs definition and solution analysis

- Allowing all participants to have a targeted, personalized experience backed by the power of local community connect

In its simplest form – along an ecosystem maturity curve – the “Social Face” of the bank can be viewed as a combination of socially integrated web and mobile toolkits that bring together the most common activities of the consumer. Personalization and targeting in the community will be brought about by segmentation based on type (e.g. commercial, personal) and level (e.g. premium) of products held aided by social, regional and demographic intelligence.

In its simplest form – along an ecosystem maturity curve – the “Social Face” of the bank can be viewed as a combination of socially integrated web and mobile toolkits that bring together the most common activities of the consumer. Personalization and targeting in the community will be brought about by segmentation based on type (e.g. commercial, personal) and level (e.g. premium) of products held aided by social, regional and demographic intelligence.

Different segments will make up the community. For example one segment may access their social causes and campaigns at both local and national levels, another may meet as a group and benchmark their upcoming travel and holiday purchases, while a third segment may monitor their social networks while reviewing their accounts to plan and review their financial goals for education or retirement. In addition, such an ecosystem also brings together third parties like health and fitness providers, non-profits, professional or family organizations and connects them through an appropriate fitment of their product offerings and transactional needs, thus boosting the payments and loyalty verticals of the bank. In fact, the various online shopping malls initiated by the banks are examples of a promising channel. But the lack of integration of this channel to the overall ecosystem relegates the value benchmarks to “price” and “discounts”. It thus leaves the door wide open for competition to venture in and break down the fragile walls of the fortress.

How does an ecosystem help engagement and financial drivers?

First, the partnership, which is based on the customers’ trust of the bank for advice will be enhanced through the arrangement of offerings around customers’ needs, backed by the views and opinions of the community itself. In other words, the aim of all but eliminating external reinforcement – the most deadly cause for loss of customer engagement today – will be fulfilled.

Second, switching costs, one of the primary methods to increase retention will raise a notch above common tools in use today. The premise is that as customers work off checklists, computations, wish-lists and plans within the ecosystem, the threshold to switch is reduced. Of course, the threshold to enter into the ecosystem is similarly high and must be created with care in an incremental fashion to make it easier for customers to adopt the ecosystem. Also obvious is that the switching costs must not be built in a way so as to inhibit the customers’ voluntary movement out of the ecosystem and into a competing ecosystem. True customer partnership implies that we are willing to let go. And even though it seems contradictory, informed self-selection often promotes growth and profitability. That’s what branding and positioning is all about – focus.

Third, a self-sustaining ecosystem will gradually be built as both individuals and other third parties in the ecosystem try to maximize their own returns. These are through campaigns, social leadership aspirational ladders, integrated banking and related non-banking products and a myriad of other ways limited only by imagination and the sanctity of the ecosystem. A little initial push in the right direction will set this off.

These are but a few of the characteristics of ecosystem development which focus on the goal of putting the bank at the forefront of the channel war, addressing the full spectrum of use cases and needs through a partner ecosystem thus minimizing the threat of being relegated as a commodity service provider. One may, of course, visit more than one community as banks and partners compete, but the share of wallet will go to the one who wins by keeping the user’s (customers, consumers and partners) needs in the forefront while constantly aligning and positioning their offerings to both expressed as well as latent needs discovered through the community interaction.

In other words, once you’re in, you’re family.

PS: You can read more about the 5 principles I followed here. They form the core of my upcoming book due in July 2014.